Daily Update - July 14th, 2026

AI's appetite continues to impact memory, power, and foundry markets

Datacenter appetite for DRAM just pushed Q2 smartphone shipments to a 13-year low. Meta’s 5GW, $50B+ Louisiana campus shows grid access is still a serious constraint. TSMC rode AI to a 36% YoY jump in June. And China keeps scaling DRAM and GPUs as export controls tighten.

AI continues to make the economics of memory and power an interesting storyline.

Let’s get into it. — Austin & Vik

Be sure to check out the Semi Doped podcast on YouTube or your favorite podcast player.

AI Memory Crunch Drives Smartphone Shipments to 13-Year Low

The concentration of DRAM capacity into high-bandwidth memory for AI accelerators is depleting supply for commodity applications, pushing global Q2 smartphone shipments to their lowest level in 13 years (Reuters).

Samsung and Apple — large enough to secure allocations — bucked the trend and gained market share while the shortage is opening a lane for Chinese upstart CXMT, whose IPO is set for July 27.

AI is simultaneously rewarding a narrow set of suppliers: HBM tooling maker Hanmi Semiconductor posted a record 52% operating margin in Q2 on surging HBM4 equipment orders (Seoul Economic Daily), even as SK Hynix equity absorbed sharp selling pressure from the bifurcated demand picture Bloomberg.com.

Here are some signals to pay attention to:

Global smartphone volumes fell 4% year-over-year in Q2 2026 to a 13-year low, with the memory chip crunch cited as the primary constraint on handset production (Reuters, Light Reading).

Samsung gained 2 percentage points and Apple gained 4 percentage points of smartphone market share versus Q2 2025, retaking leadership positions as smaller OEMs struggled to secure DRAM allocations

CXMT is on track to match Micron’s DRAM manufacturing capacity by end of 2026 (TechPowerUp), with analysts identifying the company as the primary beneficiary of mobile DRAM shortages created by HBM supply concentration9 (CNBC).

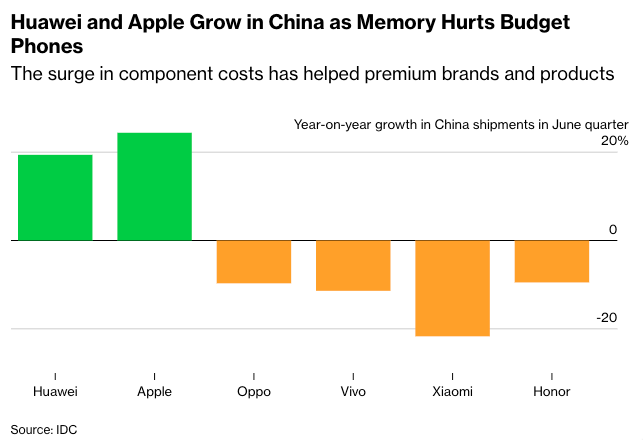

Huawei and Apple are receiving an additional lift in China specifically from the memory crisis, which is constraining rivals’ handset output, per IDC data (Bloomberg.com) — see chart below.

Kioxia shares dropped 40% amid the broader sector selloff and intensifying competition from YMTC, even as the company shipped next-generation AI memory samples aimed at closing the gap with Korean rivals (Chosun).

Vik: If AI is hitting consumer memory hard, its no wonder that smartphone sales are slumping. Plus, they’re not as sexy anymore. Your phone works, and its mostly a solved problem save for some feature frills. AI is where the hot money is at. But as expected, Apple and Samsung can absorb DRAM costs and stay afloat in the premium tier more than low end phones can.

Austin: I have a lot of thoughts and questions here!

Re: Apple and Samsung. Scarce commodity DRAM goes to the highest bidder, and a $1,000 phone can outbid a $200 phone for the same memory because that memory is smaller percentage in a premium BOM than a budget one. So premium makers win allocation because they can pass the cost through; the budget OEM gets outbid and then has to eat the margin, hike retail massively, or just not build the phone… all of which bleed share.

And part of the “share gain” could just be arithmetic… when the bottom of the market evaporates, flat premium volume becomes a bigger slice of a smaller pie, so the survivors look like winners partly because the denominator shrank.

Re: Kioxia — NAND market has many competitors, and YMTC is growing in strength. I wonder when consolidation will happen? Maybe not right now during the AI boom. But has to happen right? Kioxia + Sandisk?

China Scales DRAM and GPU Push as U.S. Export Controls Expand

China’s AI semiconductor buildout is advancing simultaneously across memory, compute, and political commitment as Washington moves to contain it through tighter distributor controls and potential model-access curbs. Nvidia has halved its approved Asian distributor list (Reuters), and the U.S. is exploring restrictions to block Chinese labs from training AI on American models (Bloomberg.com).

Apart from CXMT being on track to reach Micron-scale DRAM capacity, here are some additional points to note:

Huawei’s reported entry into DRAM production (SDxCentral) would add a vertically integrated memory player to China’s AI hardware stack, reducing dependence on CXMT as the sole domestic source.

Dongfang Suanxin’s roadmap targets Nvidia’s market position using chip architectures explicitly designed to avoid the advanced manufacturing nodes subject to U.S. export controls; the firm is backed by state funds and domestic tech companies (SCMP).

Vik: Tau Scaling is not a cure all as we all might already imagine. Quote from the SCMP article:

“Despite the optimistic road map, Wei conceded to reporters that 3D stacking was not a cure-all.

Stacking multiple silicon layers often degrades manufacturing yields, he said, while limited access to advanced fabrication nodes – the specialised foundries required to print microscopic transistors – remains the domestic industry’s fundamental constraint and ultimate performance ceiling.”

Meta’s 5GW Louisiana Campus Puts Grid Access Ahead of Silicon

Meta has expanded its Hyperion data center campus in Louisiana to 5GW of planned capacity, with total investment crossing $50 billion (Reuters, WSJ) — a single-site commitment that crystallizes grid access, not chip supply, as the binding constraint on hyperscale AI infrastructure. Meta’s Hyperion build-out in Richland Parish draws on generous Louisiana tax incentives (CNBC). Bloomberg reported the campus total cost could surpass $250 billion when long-term operational expenditures are included (Bloomberg.com).

The announcement lands as GE Vernova’s gas turbine order book is sold out through 2030 (eciks.org), Nvidia-backed Nscale’s £2 billion UK data center is stuck in a grid connection queue (Sifted), and the White House is preparing to convene utilities and data centers around a pledge on AI power costs (Reuters).

Vik: If Zuck’s dropping a quarter-trillion on a single datacenter, can you really blame Meta for wanting to sell some of that compute to make a little money back? And look at that picture! Imagine how much of that spend actually goes into building the thing versus just… buying memory. Crazy times.

Austin: Meta’s compute allocation is a portfolio decision, same as Microsoft, AWS, or GCP. Every allocation slice gets judged on ROI, risk, and time-to-cash:

1) Rent it out as a CSP. Sell capacity on the open market for the fastest payback. Smaller margins, but money in the door now.

2) Feed the ads business. Takes a bit longer to return, but the margins are much better.

3) Bet on the future. LLM-enabled features where the ROI isn’t clear yet and the risk is highest, but the biggest upside if it hits.

TSMC Revenue Surges 36% as Google Pixel 11 Allegedly Leads 2nm Ramp

TSMC reported a 36% year-over-year revenue surge in June (Bloomberg.com), setting up what analysts expect to be the company’s fifth consecutive record quarter as AI accelerator demand continues to drive advanced-node utilization (Reuters).

Simultaneously, the company’s N2 process is entering volume production with Google as its first mobile customer: the Pixel 11’s Tensor G6 chip is rumored to be the first 2nm smartphone SoC to market (GSMArena.com, 9to5Google), beating Apple’s iPhone 18 to the node by a product cycle (Notebookcheck).

In the competitive framing, Japan’s Rapidus has publicly offered 2nm wafers at ¥3.5 million (~$21,000 USD) per wafer in an explicit low-price positioning, though industry observers cited in foreign media coverage argue that price alone is unlikely to dislodge TSMC given its process maturity and customer lock-in.

Austin: Hey Rapidus, Vik and I happy to come take a tour, just send us a note!