Daily Update - July 17th, 2026

Moonshot AI released Kimi K3, market sells the news, mobile handset makers withdraw from markets, and AI making chips now?

Good Morning, it’s July 17th, 2026.

It’s all about Kimi K3 — the newest Chinese open-weight model from Moonshot that’s rattling the AI world. Lots of back-and-forth arguments about whether this model is good for the AI hardware buildout or not.

Let’s get into it. — Austin & Vik

Kimi K3 Open-Weight Release Deepens Chip Selloff, Rattles Capex Case

Following last issue’s coverage of Thinking Machines’ Inkling, a second open-weight shock hit markets: Moonshot AI’s Kimi K3, a Chinese 2.8-trillion-parameter model released July 16 that DigiTimes and SCMP say matches Anthropic’s top proprietary tier, with full weights due July 27.

The release, framed at Xi’s WAIC as a sovereign-AI push, Bloomberg reports triggered a broad chip selloff as investors again questioned whether hyperscaler capex can be justified against falling model costs.

Asian chip stocks fell sharply as the K3 news compounded existing TSMC-driven anxiety, per Bloomberg, Reuters.

Xi’s WAIC keynote—his first—explicitly championed low-cost, open AI and unveiled a 29-nation China-led AI governance body, per Bloomberg, SCMP.

TSMC maintained AI demand runs three more years Bloomberg, directly countering the selloff narrative.

K3’s full weight release July 27 is the next hard checkpoint: if benchmark scores hold on independent evals, pressure on US proprietary-model and high-end chip valuations intensifies into Q3 earnings season.

David Sacks@DavidSacksThis is concerning. For the first time, a Chinese model Kimi K3 has taken #1 on the Frontend Code Arena and is scoring at or near the frontier on other benchmarks. Meanwhile America is tying itself in knots: politicians and bureaucrats are banning new data centers, piling on

David Sacks@DavidSacksThis is concerning. For the first time, a Chinese model Kimi K3 has taken #1 on the Frontend Code Arena and is scoring at or near the frontier on other benchmarks. Meanwhile America is tying itself in knots: politicians and bureaucrats are banning new data centers, piling on Arena.ai @arenaBig news: Kimi-K3 by @Kimi_Moonshot is now #1 in the Frontend Code Arena with 1679 pts, surpassing Claude Fable 5. This is a 17-place jump from Kimi-k2.6 (#18 -> #1). In Frontend, Kimi-K3 ranked #1 in 6 of 7 domains: Brand & Marketing, Reference-Based Design, Data & Analytics, https://t.co/Oa6teaQnWp12:19 PM · Jul 17, 2026 · 30.5K Views43 Replies · 55 Reposts · 352 Likes

Arena.ai @arenaBig news: Kimi-K3 by @Kimi_Moonshot is now #1 in the Frontend Code Arena with 1679 pts, surpassing Claude Fable 5. This is a 17-place jump from Kimi-k2.6 (#18 -> #1). In Frontend, Kimi-K3 ranked #1 in 6 of 7 domains: Brand & Marketing, Reference-Based Design, Data & Analytics, https://t.co/Oa6teaQnWp12:19 PM · Jul 17, 2026 · 30.5K Views43 Replies · 55 Reposts · 352 Likes

Vik: For many people new to investing in semiconductors, it might have seemed a year ago that the only way for stocks to go is up. AI bulls will call this a buying opportunity. AI bears will interpret this as dark clouds forming where open Chinese models can provide better value per token. These frontier models are still training on NVIDIA hardware from what I can tell. Now what do we think about Jensen’s argument to sell hardware to China? Something to think about. Also read: Gavin Baker’s X post.

Austin: I don’t understand how Kimi is bad for semis. Think about it. Groq and Cerebras were dead in the water until open-source Llama came along. Open weights create incremental hardware demand… more frontier models running on-prem, more neoclouds selling models-as-a-service, more startups building products that don’t live or die on Sam or Dario’s whims.

The only companies that should be worried aren’t even public yet. Open weights are a healthy counterweight to a world where a few billionaires control our destiny.

Ask Japan…. they just ordered 27,500 Rubins to run their own models!

TSMC Raises 2026 Capex Ceiling to $64B-Plus as Market Sells the News

Following last cycle’s $265B US commitment and 77% profit jump, TSMC guided Q3 revenue to $44.6–45.8B — a sequential record — and lifted full-year revenue growth above 40%, while raising 2026 capex above $64B (Taipei Times, EE Times). Markets sold it anyway, dragging chip stocks broadly lower on margin and spending concerns.

CoWoS capacity remains “extremely tight” even as OSAT partners ramp; TSMC’s C.C. Wei welcomed competing packaging solutions as demand relief, not a threat.

Vik: TSMC posts good earnings, and a good outlook, but market sells anyway. The source of the AI buildout today is TSMC, because everything is downstream from there. When TSMC is saying they’re investing more CapEx, the market does not seem to use that as an indicator of the health of the AI hardware buildout anymore.

Austin: Notice what Wei is doing here. He welcomed Intel’s EMIB winning Google’s TPU v9, even at a reported 40 to 50% cost advantage. Why? Because the die inside that package is still almost certainly a TSMC wafer.

Packaging is the complement; wafers are the moat.

Meanwhile, ASE and SPIL are spending a record $7B of their own CapEx this year, across 15 new facilities, to reduce the CoWoS bottleneck. TSMC benefits without spending a dime.

“But isn’t packaging getting harder than ever?” Yes, agree, and that’s the point. As packaging gets harder, it looks less like assembly and more like wafer fabrication. Hybrid bonding is a cleanroom process, not a pick-and-place line. So TSMC keeps SoIC and the 3D frontier in-house, and franchises yesterday’s frontier to the OSATs. Keep the complex stuff in house, that’s the moat.

Memory Crunch Spreads From Phones to Servers as Lead Times Hit 40 Weeks

After pushing smartphones to multi-year lows, the AI memory squeeze has reached enterprise infrastructure: Inventec warns server memory lead times have exceeded 40 weeks, with shortages potentially lasting into 2028.

Micron is locking in supply through 16 Strategic Customer Agreements, including 7 automotive partners — Qualcomm, Visteon, and Harman among them.

PC brands are extending CXMT orders through end-2027 as DDR5 server demand drains available capacity across the stack.

OnePlus exits North America and Europe entirely; Oppo also suspends Realme in China — margin casualties of rising component costs.

Micron SCA auto certifications close Q3 2026; watch whether Apple holds pricing at its next supply negotiation round as the last major consumer holdout.

With CXMT’s $8.6B IPO now priced, Financial Times reports that House lawmakers have urged the Trump administration to ban US purchases of Chinese memory chips, citing national-security risk and warning that every purchase subsidizes the PLA.

Vik: Memory prices are wreaking havoc on mobile handset companies. If the entire hardware industry is being held at gunpoint with AI memory demand, something has got to give, at some point. This cannot go on forever. Consumers buying consumer hardware is equally important for the industry. AI buildout alone cannot sustain this carnage.

Key Data

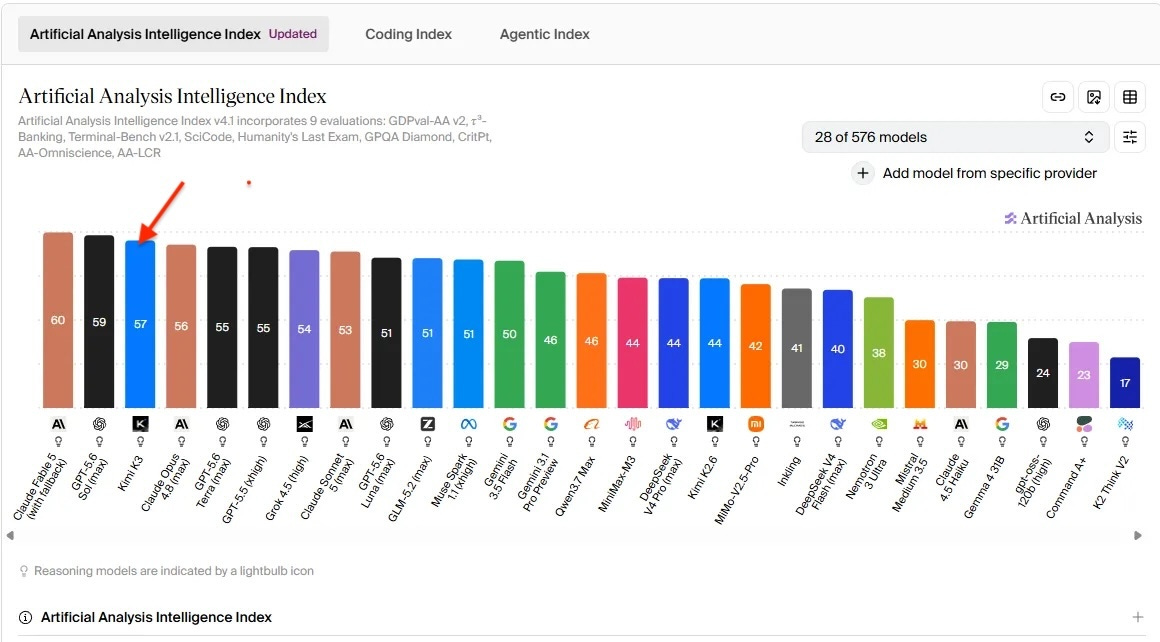

Kimi K3 at #3.

Two Days to Design a Chip — Kimi K3

“As an early proof of concept, Kimi K3 designed a chip to serve a nano model built on its own architecture. In a single 48-hour autonomous run, K3 built, optimized, and verified the chip using open-source EDA tools on the Nangate 45nm library. Within 4 mm², the chip closes timing at 100 MHz and sustains over 8,700 tokens/s decode throughput in simulation, packing 1.46M standard cells, 0.277 MB of SRAM, and an INT4 MAC array with fused dequantization. A chip built by a model, for a model, reflects K3's long-horizon agentic capabilities.”

Vik: Nice proof of concept. Not built on a leading edge node, so can’t fab this thing and expect frontier performance. It is still cool that this can actually be done agentically.

Quick Hits

Powertech and Broadcom formed a $400M Singapore joint venture targeting fan-out panel-level (FOPLP) advanced packaging for AI ASICs. (DigiTimes)

Micron signed strategic long-term supply agreements with 16 key customers including Qualcomm and seven automotive tier-1 suppliers for smart-vehicle memory. (DigiTimes)

Cadence launched AuraStack AI Super Agent, billed as the first agentic AI platform for PCB and advanced-package design, and partnered with Rapidus on SoC design. (Rutland Herald, New Electronics, DigiTimes)

Bloom Energy secured $1.7B from IDF and Oaktree to deploy fuel cells powering Nebius AI data centers in the US. (Energy Monitor, Data Center Dynamics, Fuel Cells Works)

Kioxia was hit with a $229M US jury verdict for infringing Viasat flash-memory patents, as Samsung faces a parallel Netlist ITC probe. (Reuters, TrendForce)

Mitsubishi Electric is reportedly exploring a power-chip merger with Rohm and Toshiba to consolidate Japan’s power-semiconductor sector. (Bloomberg.com)

NVIDIA launched an expanded Jetson Thor lineup (T3000/T2000) and Cosmos 3 Edge, alongside Japan’s national AI infrastructure using 27,500 Rubin GPUs. (ServeTheHome, NVIDIA IR)